Petroleum products pricing isn’t as simple as supply and demand

July 7th, 2022

Refinery capacity plays a key role in petroleum market dynamics

Prices for all sorts of commodities took off as the pandemic set in—we all heard the stories about would-be homeowners walking away from half-finished houses—and petroleum wasn’t immune to this trend. Although the spot price for West Texas Intermediate dropped like a rock throughout March and April of 2020, the price recovered quickly and was closing in on $50 per barrel by the end of that year and nearly $80 per barrel by the end of 2021. The price decrease early in the year was driven in part by a drop in demand for gasoline as many of us drove a lot less in the early days of the pandemic, and in part by speculative trading. As the nature of the pandemic became clear and we resumed normal activities, driving picked up and the market stabilized.

Putin’s misadventure in Ukraine added another $45 or so to the price early in 2022, although it has since settled down a bit, trading between $100 and $120 per barrel throughout the spring and early summer.

But the price isn’t strictly determined by the crude oil supply on one side and demand for petroleum products on the other. In between the supply and the demand is the refining industry, and it plays a key role. Crude oil is useless; it has to be turned into something else to give it real value. And, as has been widely reported over the last month or so, the U.S. has little excess refining capacity. Let’s put some numbers to demand for petroleum and the amount of U.S. refining capacity.

The Role of Refineries

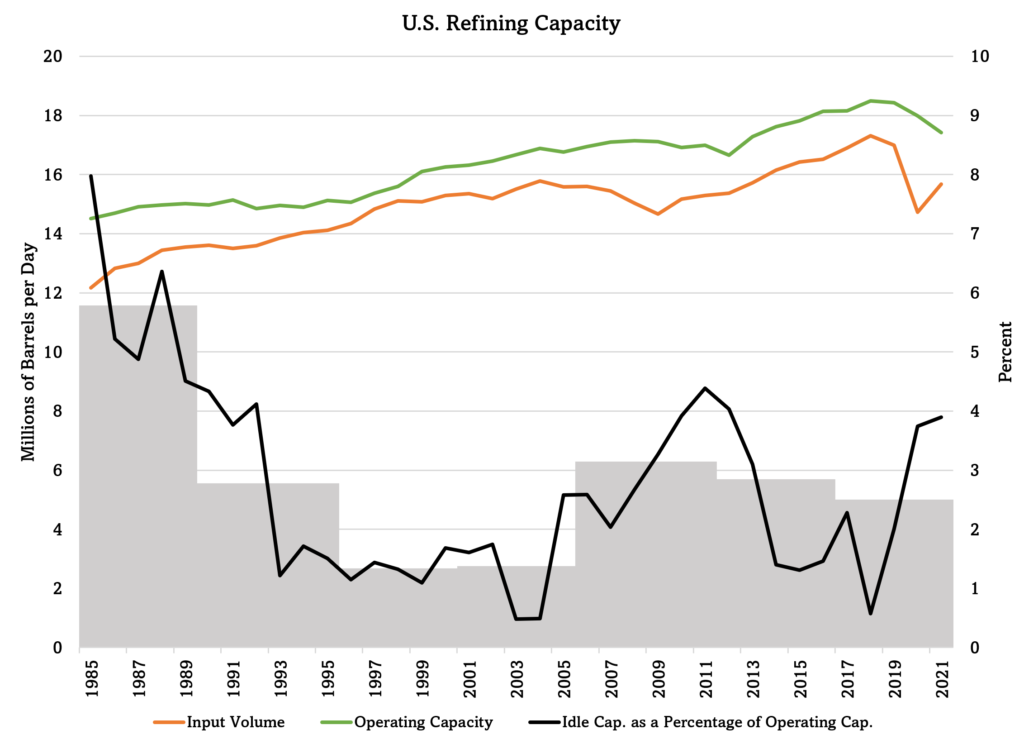

Let’s start in 1985. The demand for refined petroleum products increased from 12.2 million barrels per day in 1985 to 15.7 million BPD in 2021, an increase of 29%. However, the refinery operating capacity didn’t grow as much, increasing 22% over the same period. During this time the amount of idle capacity, as a percentage of operating capacity, fell by half. Idle refinery capacity was 5.8% in the 1985-1989 timeframe and 2.5% in the 2017-2021 period. Imagine running your business at about 94% of its capacity for years and getting it up to 97.5% of full throttle as the decades passed. That doesn’t leave much latitude for scheduled or unscheduled downtime, does it?

Relief is not in sight. Whether a refinery project involves new construction or an expansion of an existing plant, this sort of venture many challenges, including financing, regulatory hurdles, and public backlash. These projects are prohibitively expensive and many investors shun them because they often draw public ire. Closely related is the perceived risk. Given the public’s growing interest in renewable fuels, investors are wary that the ROI might be slow to materialize if alternative fuels get more traction.

While transitioning away from fossil fuels might seem like a good idea, it’s not a simple matter for a few simple reasons. People can clamor for renewables all they want, but substantial change is a long way off.

First, the U.S. has spent the last hundred years building an economy that relies in large part on petroleum. The U.S. has 4% of the world’s population yet uses 20% of the world’s crude oil. Petroleum is used mainly for transportation (66%), but indeed many industrial processes and commercial products rely on petroleum as a feedstock (28%). Petroleum has a tight grip on our economy, one that won’t loosen anytime soon.

Second, nothing compares to the energy density of gasoline. A pound of gasoline provides 18,000 British thermal units of energy. The admittedly tiny Chevrolet Spark—the least expensive gasoline-powered car on the market—has a price tag of $15,000 and gets 33 miles per gallon (city and highway combined). Its admittedly tiny fuel tank holds 9 gallons, so it has a range of approximately 300 miles. You can’t beat that. The Nissan Leaf, the least expensive electric vehicle on the market, costs $27,400 and has a range of 150 miles. Who wants to pay almost twice as much and stop twice as often to refuel? Electric vehicles are making headway, and certainly they have other benefits, but the market share is still tiny. Fewer than 1% of all the passenger vehicles in the U.S. are electric.

The Urgent Need for More Refining Capacity

Back to the refineries. It’s a point of pride that we don’t want the USA to turn into Iran. That’s right … Iran! That nation sits on vast natural reservoirs of oil, the fourth largest source of proven oil reserves, a resource eclipsed only by its vast reservoir of industrial ineptitude. For decades Iran’s refining capacity was so undersized and decrepit that it had to import gasoline. Exporting raw materials and importing finished goods is the pinnacle of poor planning, and Iran excelled at it. A few years ago the nation managed to turn its situation around when it completed the Persian Gulf Star Refinery, an investment of $3.4 billion. Completed in 2018, it finally allowed Iran to declare that it was self-sufficient in gasoline production.

If we find ourselves too hemmed in by the political will of the alternative energy crowd and burdensome regulations, two things will happen. First, the world’s largest oil producer and consumer will run out of refining capacity. Second, the USA will be outclassed by Iran.

Sources: The Energy Information Administration (www.eia.gov), American Fuel & Petrochemical Manufacturers (www.afpm.org), Reuters (reuters.com), hydrocarbons-technology.com, Edmunds (www.edmunds.com), motor1.com.

Recent Posts

Snapshot – April 2024

Interest rates: The benchmark federal interest rate, the Federal Funds Rate, …Read More »Insights – April 2024

Interest rates: The benchmark federal interest rate, the Federal Funds Rate, …Read More »Inflation and energy prices to choke Europe’s growth engine

Inflation, especially regarding the cost of energy, is a big …Read More »Oil prices have fallen but remain volatile

Since the middle of June, oil prices have fallen more …Read More »Developing shorter supply chains, strengthening domestic manufacturing

Anyone familiar with a pendulum’s action knows how business trends …Read More »